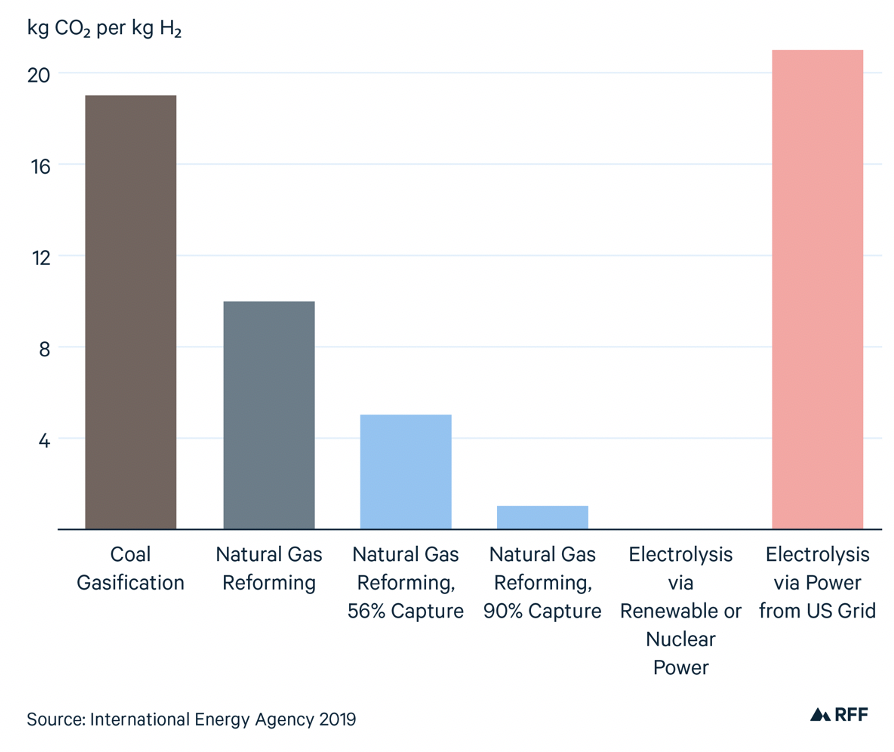

Rather than using fossil fuels as the source of hydrogen atoms and reaction energy, the production of green hydrogen involves splitting water through the use of electricity generated by nuclear or renewable energy. For electrolytic hydrogen to be green, the power must be from zero-carbon generation. As shown in Figure 1, producing hydrogen through electrolysis using US grid electricity would, on average, result in higher emissions than the production of brown hydrogen.

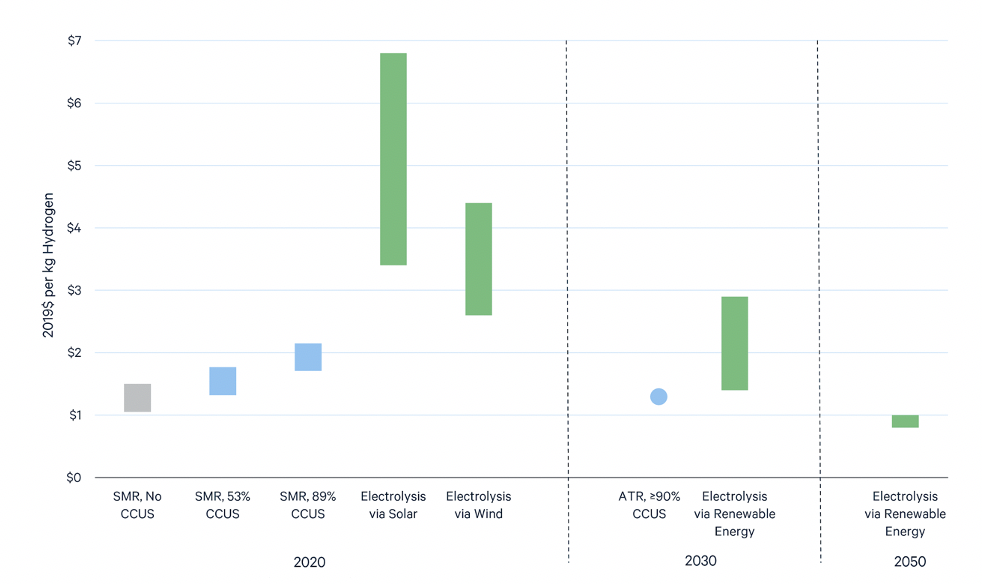

As Figure 2 makes clear, green hydrogen is significantly more expensive than blue hydrogen to produce, even though the fixed costs—capital and fixed operating costs—of blue hydrogen are higher than those of green hydrogen, and the processes to produce both blue and green hydrogen involve similar energy efficiencies. This disparity in production costs is due to two factors. First, the energy cost for electricity is much higher than for natural gas. On an energy basis, $3.50 per million British thermal units for natural gas is equivalent to $12 per megawatt hour (MWh) for electricity, which compares with current costs of $30–$40 per MWh for wind and solar power, before subsidies. Second, because green hydrogen production is limited by the availability of zero-carbon power, it operates only a fraction of the time. Consequently, although the capital cost per megawatt of green hydrogen capacity is less than that of blue hydrogen, low utilization causes the capital cost per kg H₂ to be higher for green hydrogen than for blue hydrogen.

Reducing the cost of green hydrogen thus hinges on lower power costs and lower capital costs per kg H₂. In optimal locations, solar and onshore wind power costs may decline to about $25 per MWh in 2030 and $15 per MWh in 2050. Increases in utilization are constrained by the capacity factors of wind and solar energy, but combining wind and solar in locations where their generation profiles are complementary, or including battery storage, could help produce more green hydrogen. Although nuclear power would provide continuous energy, it is too expensive to enable competitively priced green hydrogen. Capital costs per kg H₂ would also decrease with lower electrolyzer costs, which could decline significantly through increased manufacturing scale and automation. Indeed, electrolyzer costs are projected to decline as much as 90 percent by 2050, although much uncertainty exists about whether these reductions will prove feasible. If such low costs are achieved, producing green hydrogen would cost less than gray hydrogen, even before accounting for CO₂ emissions.

For an oil refinery or ammonia plant, the delivered cost of hydrogen is more relevant than its production cost. Unless hydrogen is produced on-site, the delivered cost also includes transportation and storage costs. Because hydrogen has a very low density and the potential to embrittle steel, storage and pipeline costs are considerably more expensive for hydrogen than for natural gas. Salt cavern storage, the least expensive option for hydrogen, may cost $0.11–$0.23 per kg H₂, and hydrogen pipeline transport may cost $0.05–$0.10 per kg H₂ for every 100 kilometers. Even with optimal storage and over small distances, transportation and storage costs would add significant expense to the delivered cost of hydrogen.

As a feedstock for US oil refining and ammonia production, blue hydrogen is likely to incur lower transportation and storage costs than green hydrogen for two reasons. First, abundant natural gas, salt cavern storage, oil refineries, and ammonia plants are all present along the Gulf Coast, along with an existing hydrogen pipeline network, which would minimize the delivered cost of blue hydrogen. In contrast, the least expensive green hydrogen production would occur in the Great Plains (with wind power) or Southwest (with solar power), both of which are regions that have more dispersed oil refining and ammonia production and less developed salt cavern storage. Second, blue hydrogen production can run nearly constantly, so it requires only a modest amount of storage and can be produced on-site at oil refineries or ammonia plants. Conversely, green hydrogen production is limited by the availability of low-cost, zero-carbon power, which will vary on a daily and seasonal basis. Therefore, significant amounts of storage would be needed to ensure a steady supply of green hydrogen for oil refineries and ammonia plants.

In the near term, blue hydrogen is the more cost-effective method for reducing carbon emissions in oil refining and ammonia production, but green hydrogen offers a longer-term pathway to decarbonized hydrogen, with the advantages of minimal emissions and a production cost that does not depend on natural gas reforming. The cost of green hydrogen production, transport, and storage must decline substantially for green hydrogen to competitively supply feedstock for oil refining and ammonia production. As with blue hydrogen on the Gulf Coast, or the proposed green hydrogen–based energy storage project in Utah, locating feedstock demand near salt cavern storage and in regions that boast excellent solar or wind resources would facilitate industrial use of green hydrogen.