| 来源类型 | Policy Contribution |

| 规范类型 | 简报 |

| The European Central Bank’s quantitative easing programme: limits and risks | |

| Grégory Claeys; Alvaro Leandro | |

| 发表日期 | 2016-02-15 |

| 出版年 | 2016 |

| 语种 | 英语 |

| 概述 | The ECB has made a series of changes to its QE programme in order to expand the universe of purchasable assets and have more flexibility in the execution of the programme. However this might not be enough to sustain QE throughout 2017. The extension of the programme also raises questions about its potential adverse consequences. |

| 摘要 | Highlights

EXECUTIVE SUMMARY

1. IntroductionOn 22 January 2015, the European Central Bank (ECB) introduced the Public Sector Purchase Programme (PSPP). Under the PSPP, the Eurosystem started in March 2015 to buy sovereign bonds from euro-area governments and securities from European institutions and national agencies. On 3 December 2015, ECB president Mario Draghi announced an extension of the programme. While it was initially foreseen to last until at least September 2016, it was extended until at least March 2017. Additionally, regional and local government bonds were added to the list of eligible assets for purchase, and the interest rate on the deposit facility was lowered from -0.2 percent to -0.3 percent. President Draghi said that the asset purchase programme would continue “until we see a sustained convergence towards our objective of a rate of inflation which is below but close to 2 percent” (Draghi 2015c). This goal remains far from being fulfilled: euro-area year-on-year headline inflation has been below 2 percent since January 2013, below 1 percent since November 2013, and was still at 0.2 percent in December 2015, while core inflation was only at 0.9 percent. In the meantime, and most importantly, both medium- and long-term market-based expectations and inflation forecasts have started to fall again (Figure 1). As both measures suggest, after a clear decline until the end of 2014, inflation expectations rebounded significantly after QE was announced in January 2015 and during the whole first half of 2015. However, expectations recently fell back to previous lows, heavily influenced by the steep decline in oil prices, as explained in Darvas and Hüttl (2016). Figure 1: Market-based and survey-based inflation expectations in the euro areaSources: Thomson Reuters Eikon (left panel) and ECB Survey of Professional Forecasters (2016) (right panel). Note: HICP = Harmonised Index of Consumer Prices.

For these reasons and because inflation appears likely to substantially undershoot the ECB’s staff forecast over the next two years, it is probable1 that the ECB will enhance its programme further in order to fulfil its mandate and bring inflation back towards 2 percent in the medium term. Even if the impact of asset purchase programmes is more difficult to measure than that of more conventional monetary measures, a growing literature2 concludes that QE programmes implemented around the world boosted inflation, output and employment. For the euro area in particular, the effects of QE are even more difficult to pin down given that the programme only started in March 2015. However, there are already some indications that QE is having some impact on the euro-area economy. The effects on the exchange rate and on interest rates (and in particular on financial fragmentation in the euro area, with credit rates converging again) have been the most visible. In terms of inflation, monetary measures take time to materialise in prices and it is very difficult to know what can be attributed exactly to QE, but, for instance, the basket share of the consumer price index in deflation declined from 40 percent at the beginning of 2015 to 25 percent at the start of 2016. Darvas (2016) also shows that core inflation adjusted for second-round effects of energy prices went up over 2015 and, after reaching a low point in Q1 2015 of around 0.7 percent, it is now at 1.2 percent, a level unseen since 2011. However desirable they might be, the recent – and maybe future – extensions of the asset purchase programme raise questions about how its size and its duration can be materially increased given the finite volume of purchasable debt securities. In fact, the universe of purchasable debt securities needs to be expanded because of the ECB’s self-imposed limit on the proportion it can hold of a given debt issue (decided at the launch of the programme) and not so much because of the scarcity of debt securities. Claeys et al (2015b) showed already at the launch of the PSPP that without any changes to the design of the programme this limit could be reached in March 2017 or before in a number of countries. For Germany, calculations in Claeys et al (2015b) suggested that the limit would be reached in April 2017. Given the structure of the programme using the ECB capital keys to determine the distribution of purchases between countries, this could have seriously limited its effectiveness. Since then, the issue share limit was raised in September 2015, and the changes to the programme in December 2015 further expanded the universe of eligible debt that can be purchased by the Eurosystem. However, these expansions might still not be enough to prevent the limits being reached before the inflation target is achieved. Furthermore, the unconventional and previously untested nature of such a programme poses legitimate questions regarding the potential adverse consequences that such a substantial and prolonged programme could have. In section 2 we explain the changes to the design of the purchase programme during its first year of implementation, and their implications for our calculations on when the limits will be reached, also envisaging a scenario in which the monthly amounts purchased under the PSPP would be increased. We then discuss potential risks that accompany a lengthy and massive asset-purchase programme in terms of inequality, financial stability and the central bank’s credibility. 2. Potential implementation limits of the asset purchase programme2.1 The extended asset purchase programme’s original guidelinesOn 22 January 2015 the ECB announced a massive expansion of its asset purchase programme. To supplement the Asset-Backed Securities and Covered Bonds Purchase Programmes (ABSPP and CBPP3) launched in September 2014, the ECB introduced a new Public Sector Purchase Programme (PSPP) to buy sovereign bonds from euro-area governments and securities from European supranational institutions and national agencies. While total monthly purchases of asset-backed securities and covered bonds had previously amounted to approximatively €10 billion per month, the new purchases of sovereign bonds, supranational institutions, and agencies raised the figure to €60 billion per month, €44 billion of which was dedicated to purchases of government and national agency bonds (and this €44 billion was divided between euro-area countries according to each country’s capital subscription at the ECB). The purchases started on 9 March 2015 and were originally meant to last at least until September 2016. The ECB’s Governing Council also made it clear at the time that the programme was open-ended and that purchases would be conducted until the ECB would see “a sustained adjustment in the path of inflation which is consistent with the aim of achieving inflation rates below, but close to, 2 percent”. On top of the eligibility criteria (ie only debt securities with a remaining maturity between 2 and 30 years and with a yield above the deposit rate can be bought), the ECB’s Governing Council also decided to put in place a 25 percent issue limit and a 33 percent issuer limit on Eurosystem holdings. The 25 percent issue limit was imposed to prevent the ECB from having “a blocking minority in a debt restructuring involving collective action clauses”. This indicated that the ECB did not wish to be in a position in which it had the power to block a potential vote on the restructuring of ECB-held debt of a euro-area country, because not blocking such a restructuring would be interpreted as monetary financing of a member state3. 2.2 Changes to the ECB’s guidelines since March 2015The ECB’s rules on the Public Sector Purchase Programme (PSPP) have gradually been adapted since the programme started in March 2015. As highlighted in Claeys et al (2015b), the original rules rapidly constrained the purchases in countries in which public debt was small and in which no national agencies were identified as eligible for purchases. The aim of most of the changes was therefore to expand the universe of available debt securities that the Eurosystem could purchase, in order to delay the point at which the programme would reach its limits in each euro-area country. In July 2015, the ECB expanded the list of national agencies whose securities are eligible for purchase under the PSPP (see Table 1), thereby allowing the Eurosystem to purchase debt securities in countries where the limits had already been reached, or were expected to be reached soon. In September 20154, the issue share limit was increased from 25 percent to 33 percent for debt securities not containing collective action clauses (CACs). This change to the maximum amount that the Eurosystem can hold of a particular issue allows the PSPP to potentially continue for longer than was originally possible under the previous rules. In December 20155, the Governing Council announced many new changes to the design of the PSPP. First, it decided to reduce the deposit rate from -0.2 percent to -0.3 percent. Since the Eurosystem decided to purchase bonds with yields above the deposit rate in order to avoid making a direct loss on the purchases6, the cutting of the deposit rate effectively increased the amount of debt securities eligible for purchase (even if the rate cut also reduced yields and therefore limited the volume increase). Second, the ECB decided to continue the PSPP past the previously-announced minimum end-date, September 2016, until March 2017, “or beyond, if necessary”. Third, euro-denominated debt issued by regional and local euro-area governments became eligible for purchase. Finally, the ECB declared its intention to reinvest the principal payments on the securities purchased under the programme as they mature, for as long as necessary. This effectively implies that in March 2017, two years after the start of the programme, when the first bonds bought by the Eurosystem will start to mature, monthly purchases of sovereign and agency bonds could exceed €44 billion, as the principals of these maturing bonds will be reinvested.

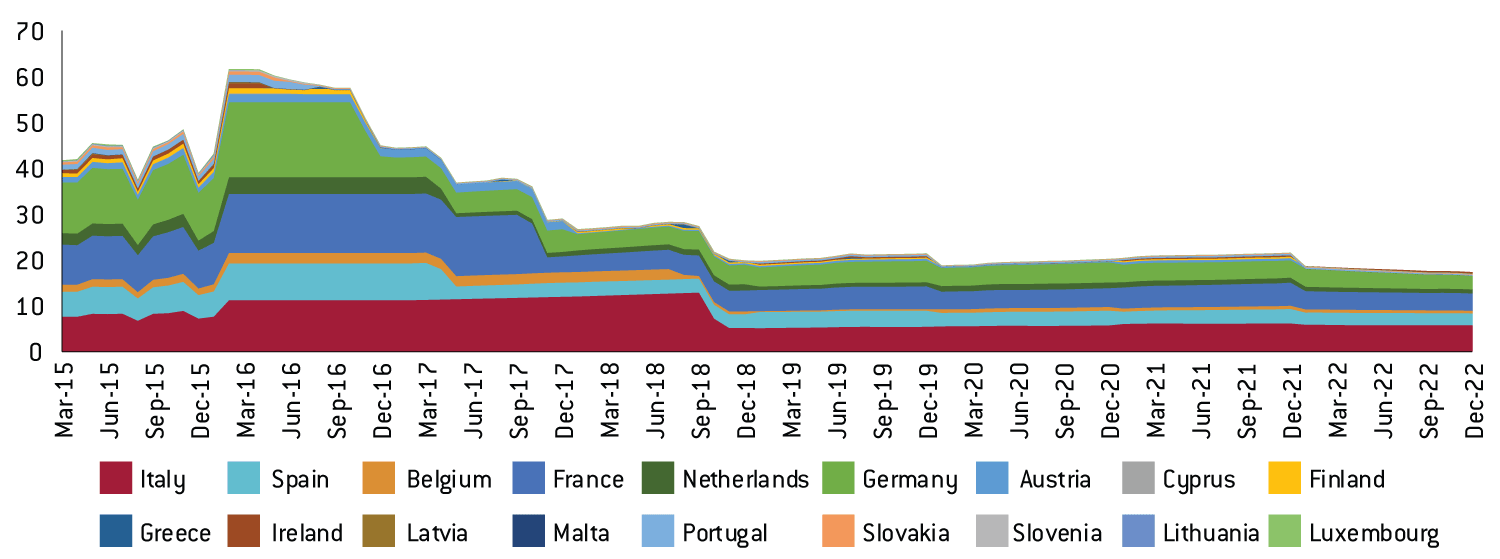

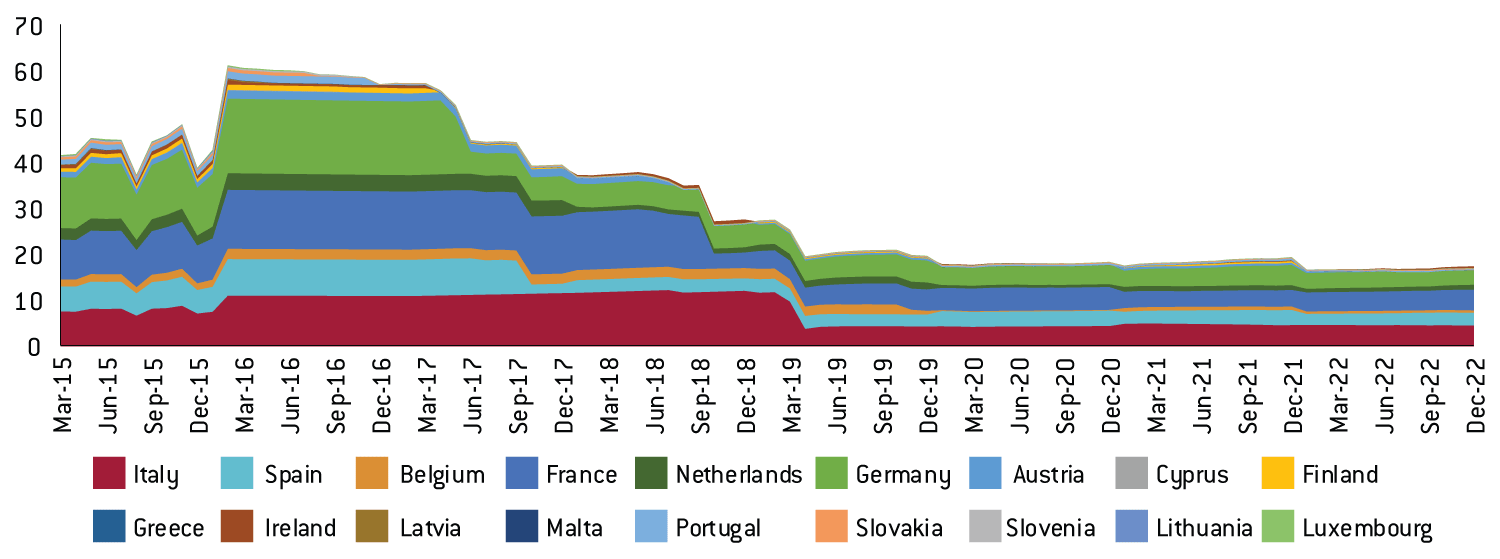

2.3 Limits of the programme in terms of size, duration and compositionClaeys et al (2015b), published at the time of the start of the purchases, calculated when the ECB’s limits would be reached in each euro-area country (Figure 2). In this section we update these calculations7 in light of the changes to the rules. We also include national agencies in our calculations8. Before September 2015 the issue limit was 25 percent regardless of the type of bond. Now, however, this limit is 33 percent if the issue does not contain a collective action clause. Unfortunately, information on whether an issue contains a CAC is not readily available. We know, however, that according to the ESM Treaty9, all euro-area government debt securities with maturity over one year issued after 1 January 2013 contain CACs. Therefore, we envisaged two extreme scenarios: in the first scenario, we assume that all eligible debt securities, be they from agencies, local governments, or central governments, have CACs, in which case the Eurosystem can only hold a maximum of 25 percent of a country’s eligible debt securities. In the second scenario, we assume that the only debt securities to have CACs are those issued by central governments after 1 January 2013 (in this scenario, the Eurosystem can hold 25 percent of each issue containing CACs, and 33 percent of each issue which does not). Reality will lie between these two extremes. Figure 3 shows our projections for the monthly purchases, by country, in the scenario in which every debt security contains a CAC. Despite the increase in eligible debt (with the expanded list of agencies, and the new ability to buy regional and local debt), the limits are reached roughly at the same time as in Figure 2, and even earlier in some cases. This is because of the reinvestment of principals, which kicks in in March 2017: it effectively raises the amounts purchased each month, and increases the speed at which the limits are reached. In fact, while redemptions of PSPP holdings will be small at first, they would accelerate quickly as more and more debt securities held by the Eurosystem mature. In Germany, for instance, the holdings maturing in March 2017 will be worth a few million euros, while, were the programme to go on until then, they will be worth roughly €1.5 billion per month in March 2019, which is sizeable because it would increase the monthly purchases of German bonds by approximately 10 percent. This effectively means that, while the limits will be reached at roughly the same time as before the rules changed, the balance sheet of the Eurosystem will be bigger at that time thanks to the increase in eligible debt. Figure 4 shows our projections for the second scenario, in which only central government debt securities issued after 1 January 2013 are assumed to contain CACs. The limits will be reached later than in scenario 1, as can be seen easily by comparing figures 2 and 3. For example, while in scenario 1, purchases in Germany are heavily constrained after April 2017, this is not the case until March 2018 in scenario 2. On 21 January 2016, President Draghi hinted at further easing, given “downside risks” related to heightened uncertainty about the growth prospects of emerging economies, volatility in financial and commodity markets, and geopolitical risks. While this further easing could come in the form of a further reduction in the deposit rate, which would increase the amount of debt eligible for purchase (provided that the yields on these securities do not fall excessively in the meantime), the Governing Council might also decide to increase the amounts purchased each month under the PSPP. The Eurosystem is currently purchasing €44 billion of agency and government debt per month, but this could be raised. In Figures 5 and 6 we show our projections of monthly purchases were the amounts purchased each month to increase from €44 billion to €64 billion in March 2016, in both scenarios. As is apparent, the limits in each country would be reached much more quickly. Under the more restrictive scenario 1, the limit in Germany, the country in which purchases are the highest, would be reached as soon as November 2016. An increase in monthly purchases might be desirable to provide immediately a more accommodative stance to the euro area’s monetary policy in order to reach the inflation target, but it might not be compatible with a longer duration of the programme if the rest of the programme design remains unchanged. Figure 2: Projection of monthly purchases (€ billion) per country with original rules (excluding national agencies) from Claeys et al (2015b)Sources: Bruegel based on ECB, NCBS, National Treasuries, Datastream. Note: Luxembourg, Lithuania and Estonia do not appear on this chart given the very small amount of debt securities of these countries in the market.

Figure 3: Projection of monthly purchases (€ billion) per country, including national agencies (scenario 1: all debt securities contain CACs)Source: Bruegel based on ECB, NCBs, National Treasuries, Thomson Reuters.

Figure 4: Projection of monthly purchases (€ billion) per country, including national agencies (scenario 2: only central government debt issued after the 1st of January 2013 contains CACs)Source: Bruegel based on ECB, NCBs, National Treasuries, Thomson Reuters.

2.4 What could be done to further extend the duration of the programme if necessary?Claeys et al (2015b) already recommended that the ECB increase the 25 percent issue limit to address the constraint that it would place on the size and duration of the PSPP. Claeys et al (2015b) also recommended that the list of eligible agencies be broadened. These changes have been put in place since March 2015, but that might not be enough to increase the pool of eligible assets. That is why Claeys et al (2015b) also recommended waiving entirely the issue limit, at least for AAA-rated bonds. This would allow, for instance, longer purchases of German sovereign bonds or European Investment Bank bonds. The composition of the purchases could also be further altered. As already discussed at length in Claeys et al (2014), there are other types of assets that the Eurosystem could purchase if the ECB QE programme needs to be enhanced to bring inflation back to target. This could lengthen the duration of asset purchases, and increase the monthly monetary stimulus. The Eurosystem could purchase senior well-rated uncovered bank bonds. While they are riskier than the covered bank bonds which are already being purchased under the CBPP3, the comprehensive assessment carried out by the ECB and national supervisors in 2014 and 2015 should theoretically ensure that euro-area banks are adequately capitalised and can smoothly absorb financial shocks. According to the ECB, there is currently more than €2 trillion of uncovered bank bonds which are eligible as ECB collateral10 (the Eurosystem collateral eligibility framework is not exactly similar but is roughly comparable to the eligibility criteria of assets for purchase, except for instance in terms of accepted maturity and minimum yield). Another possibility would be for the Eurosystem to purchase corporate bonds, of which there are almost €1.5 trillion eligible for collateral purposes (although part of these are not euro-denominated, or are issued by corporates outside the euro area, in which case they should not be eligible). Purchases of these securities might have different, or even complementary, effects, as explained in Claeys et al (2014). However, they could help the Eurosystem provide a stronger monetary accommodation for a longer period, and delay worries that the QE programme would reach its limits before the path of inflation is consistent with the inflation target. Finally, the ECB Governing Council could also decide to change the way purchases are spread across euro-area countries, in order to shift some of the purchases from countries in which the limit will be binding (eg in Germany by the Bundesbank) to other national central banks. The first major country in which the limits will be reached is Germany, because the amounts purchased in each country are proportional to the country’s capital subscription to the Eurosystem, of which Germany is the largest, while there is proportionally much less outstanding debt in Germany than in Italy, for example. Distributing the purchases across countries according to their outstanding debt instead of distributing them according to the ECB capital keys would lead to limits being reached in every country at roughly the same time11. Given the various channels through which asset purchases can influence monetary conditions and thereby economic activity and prices, changing the country distribution of purchases could alter the effects of QE in the euro area12, which should be carefully taken into consideration by the Governing Council, were it to take this decision. Figure 5: Projection of monthly purchases (€ billion) per country, including national agencies, if amount purchased is increased to €64 billion (scenario 1: all debt securities contain CACs)Source: Bruegel based on ECB, NCBs, National Treasuries, Thomson Reuters. Note: see note to Figure 3.

Figure 6: Projection of monthly purchases (€ billion) per country, including national agencies, if amount purchased is increased to €64 billion (scenario 2: only central government debt issued after 1 January 2013 contains CACs)Source: Bruegel based on ECB, NCBs, National Treasuries, Thomson Reuters. Note: see note to Figure 3.

3. Potential risks related to unconventional monetary policyThe unconventional and previously untested nature of these policies poses some legitimate questions regarding their potential adverse consequences for financial stability, inequality and in terms of the credibility of the ECB. 3.1 Risks for financial stabilityThe ECB’s asset purchase programme, combined with the other unconventional monetary measures implemented since 2008 to avoid a full-scale liquidity crisis in the banking sector and the break-up of the euro area, contributes to an accommodative monetary policy stance. Cuts to the central bank rates to close to or even below zero, large-scale asset purchases, long-maturity lending to banks and forward guidance lead to loose monetary conditions that should stimulate growth and bring inflation back towards the 2 percent target. By increasing inflation and output (and therefore public debt sustainability), these measures should benefit financial stability. However, prolonged accommodative monetary policies could also pose some challenges to financial institutions and might have adverse consequences through various channels for financial stability. One of the purposes of monetary policy is to support the economy by encouraging more risk-taking at a time when risk-taking in the financial system is less than socially desirable. However, if risk-taking becomes excessive and goes beyond what is socially desirable, it might contribute to future financial instability. It is very difficult to say when risk-taking becomes excessive, but as discussed in Claeys and Darvas (2015), banking indicators do not suggest substantially-increased risk-taking ove |

| 主题 | European Macroeconomics & Governance ; European Parliament |

| 关键词 | European Central Bank (ECB) Monetary policy Quantitative Easing |

| URL | https://bruegel.org/2016/02/the-european-central-banks-quantitative-easing-programme-limits-and-risks/ |

| 来源智库 | Bruegel (Belgium) |

| 资源类型 | 智库出版物 |

| 条目标识符 | http://119.78.100.153/handle/2XGU8XDN/429540 |

| 推荐引用方式 GB/T 7714 | Grégory Claeys,Alvaro Leandro. The European Central Bank’s quantitative easing programme: limits and risks. 2016. |

| 条目包含的文件 | ||||||

| 文件名称/大小 | 资源类型 | 版本类型 | 开放类型 | 使用许可 | ||

| 12814-000001.png(35KB) | 智库出版物 | 限制开放 | CC BY-NC-SA |  浏览 | ||

| pc_2016_04.pdf(390KB) | 智库出版物 | 限制开放 | CC BY-NC-SA | 浏览 | ||

| 个性服务 |

| 推荐该条目 |

| 保存到收藏夹 |

| 导出为Endnote文件 |

| 谷歌学术 |

| 谷歌学术中相似的文章 |

| [Grégory Claeys]的文章 |

| [Alvaro Leandro]的文章 |

| 百度学术 |

| 百度学术中相似的文章 |

| [Grégory Claeys]的文章 |

| [Alvaro Leandro]的文章 |

| 必应学术 |

| 必应学术中相似的文章 |

| [Grégory Claeys]的文章 |

| [Alvaro Leandro]的文章 |

| 相关权益政策 |

| 暂无数据 |

| 收藏/分享 |

| 文件名: | 12814-000001.png |

| 格式: | image/png |

除非特别说明,本系统中所有内容都受版权保护,并保留所有权利。